Market Overview

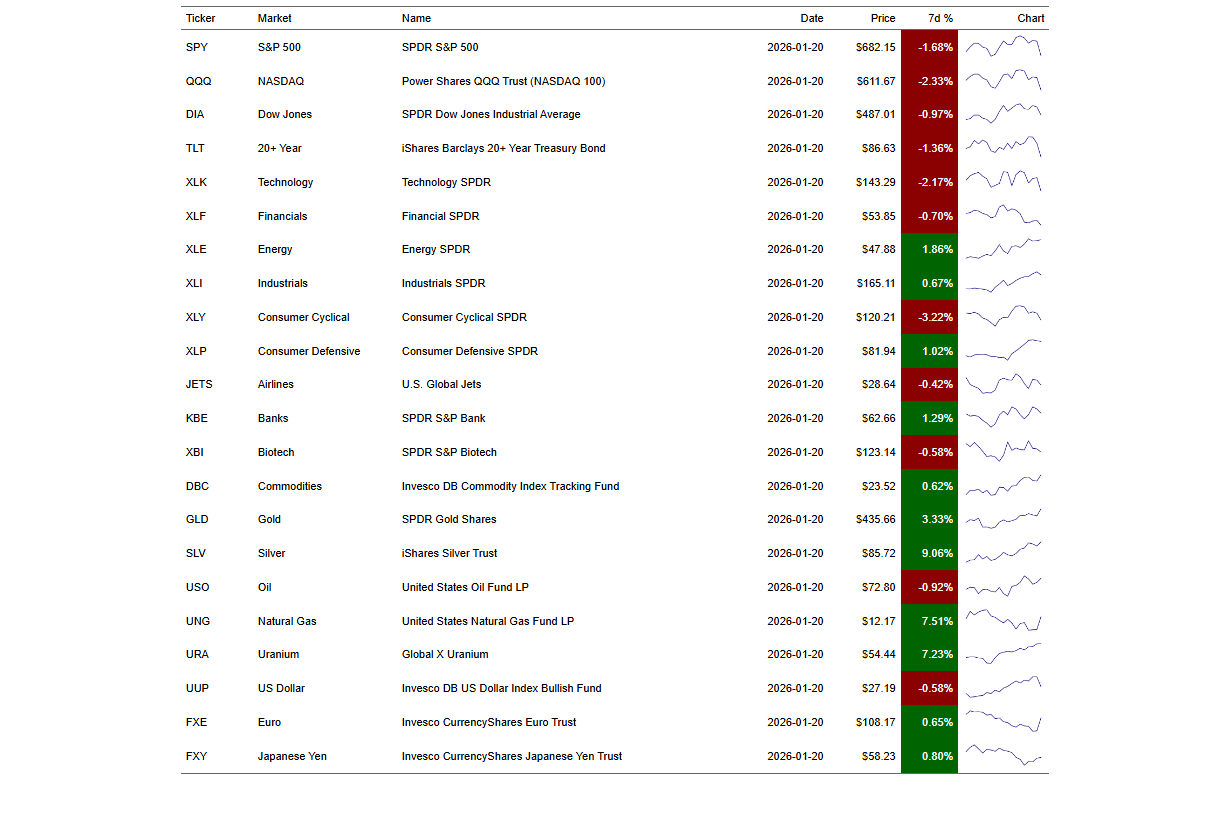

This week’s Weekly Watch highlights a notable shift in market behavior. Compared with last week’s broad participation across assets, leadership has narrowed meaningfully. Capital is no longer flowing evenly across equities, sectors, and commodities. Instead, it is becoming more selective.

The defining theme is defensive rotation combined with continued real asset leadership.

From Broad Participation to Selectivity

Last week, equities, cyclicals, commodities, and precious metals were largely moving higher together. That type of environment typically reflects rotation within risk rather than outright risk aversion.

This week looks different.

- Growth-oriented equities, particularly technology and consumer discretionary, are under pressure

- Market breadth has narrowed

- Fewer assets are carrying upside momentum

This change suggests investors are becoming more discriminating in where capital is deployed.

Defensive Assets Are Gaining Relative Strength

As equity leadership weakens, defensive sectors are holding up better on a relative basis. Consumer staples and other lower-volatility areas are showing resilience, indicating a preference for stability over growth.

Defensive rotation often emerges when investors are less confident in near-term economic acceleration but are not yet pricing in a full-scale crisis.

Real Assets Continue to Attract Capital

At the same time, real assets remain a key area of strength:

- Gold continues to act as a preferred hedge

- Silver is outperforming gold, signaling broader stress hedging rather than short-term panic

- Uranium and select commodities remain firm

When real assets outperform alongside defensive equity behavior, it often reflects ongoing macro uncertainty rather than a single shock event.

Bonds Are Not Acting as a Traditional Hedge

One important divergence this week is the behavior of long-duration bonds. Rather than providing protection as equities weaken, Treasuries remain under pressure.

This matters because it shifts the hedging role away from duration and toward alternatives such as precious metals and selective commodities.

Intermarket Interpretation

Taken together, this week’s data points to capital reallocation, not indiscriminate selling.

Key intermarket signals include:

- Weakening growth equities

- Narrowing market breadth

- Defensive sector resilience

- Persistent strength in precious metals

- Bonds failing to offset equity weakness

This combination is consistent with a late-cycle or adjustment phase, where markets reward selectivity rather than broad exposure.

What to Watch Going Forward

If this rotation persists, several signals will be important:

- Whether defensive sectors continue to outperform cyclicals

- Whether real assets maintain leadership

- Whether bonds begin to reclaim their role as a hedge

- Whether market breadth stabilizes or continues to deteriorate

These relationships will help clarify whether markets are transitioning into a more sustained defensive regime or simply pausing after last week’s broader advance.

Bottom Line

Last week reflected broad participation across markets. This week reflects defensive selectivity and real asset leadership.

That shift does not confirm a full risk-off environment, but it does suggest that investors are prioritizing protection and hedging over growth-sensitive exposure.

Monitoring these intermarket relationships over time provides more insight than any single indicator in isolation.

This content is for informational and educational purposes only and does not constitute financial or investment advice.